For a rapidly growing share of older Americans, traditional ideas

about life in retirement are being upended by a dismal reality: bankruptcy.

The signs of potential trouble — vanishing pensions, soaring medical expenses,

inadequate savings — have been building for years. Now, new research sheds light

on the scope of the problem: The rate of people 65 and older filing for

bankruptcy is three times what it was in 1991, the study found, and the same

group accounts for a far greater share of all filers.

Driving the surge, the study suggests, is a three-decade shift of financial risk

from government and employers to individuals, who are bearing an ever-greater

responsibility for their own financial well-being as the social safety net

shrinks.

The transfer has come in the form of, among other things, longer waits for full

Social Security benefits, the replacement of employer-provided pensions with

401(k) savings plans and more out-of-pocket spending on health care. Declining

incomes, whether in retirement or leading up to it, compound the challenge.

Cheryl Mcleod of Las Vegas filed for bankruptcy in January after struggling to

keep up with her mortgage payments and other expenses. “I am 70, and I am

working for less money than I ever did in my life,” she said. “This life stuff

happens.”

As the study, from the Consumer Bankruptcy Project, explains, older people whose

finances are precarious have few places to turn. “When the costs of aging are

off-loaded onto a population that simply does not have access to adequate

resources, something has to give,” the study says, “and older Americans turn to

what little is left of the social safety net — bankruptcy court.”

“You can manage O.K. until there is a little stumble,” said Deborah Thorne, an

associate professor of sociology at the University of Idaho and an author of the

study. “It doesn’t even take a big thing.”

The forces at work affect many Americans, but older people are often less able

to weather them, according to Professor Thorne and her colleagues in the study.

Finding, and keeping, one job is hard enough for an older person. Taking on

another to pay unexpected bills is almost unfathomable.

Bankruptcy can offer a fresh start for people who need one, but for older

Americans it “is too little too late,” the study says. “By the time they file,

their wealth has vanished and they simply do not have enough years to get back

on their feet.”

Not only are more older people seeking relief through bankruptcy,

but they also represent a widening slice of all filers: 12.2 percent of filers

are now 65 or older, up from 2.1 percent in 1991.

The jump is so pronounced, the study says, that the aging of the baby boom

generation cannot explain it.

Although the actual number of older people filing for bankruptcy was relatively

small — about 100,000 a year during the period in question — the researchers

said it signaled that there were many more people in financial distress.

“The people who show up in bankruptcy are always the tip of the iceberg,” said

Robert M. Lawless, a law professor at the University of Illinois and another

author of the study.

The next generation nearing retirement age is also filing for bankruptcy in

greater numbers, and the average age of filers is rising, the study found.

Given the rate of increase, Professor Thorne said, “the only explanation that

makes any sense are structural shifts.”

Ms. Mcleod said she had managed to get by for a while after separating from her

husband several years ago. Eventually, though, she struggled to make ends meet

on her income alone, and she fell behind on her mortgage payments.

She collects a small Social Security check and works at an adult day care center

for people with intellectual disabilities and mental health problems. For $8.75

an hour, she makes sure clients participate in daily activities, calms them when

they are irritated and tries to understand what they need when they have trouble

expressing themselves.

“When I moved here from Los Angeles, I was wondering why all of these older

people were working in convenience stores and fast-food restaurants,” she said.

“It’s because they don’t make enough in retirement to support themselves.”

Ms. Mcleod said she hoped that filing for bankruptcy would help her catch up on

her mortgage so she could stay in her home. “I am too old to move out of here,”

she said. “I am trying to stay stable.”

For about one in three older people who receive Social Security benefits, their

monthly check accounts for 90 percent of their income, according to the Social

Security Administration. Spending by those over 65 by income is based on

Medicare beneficiaries, most of whom are 65 and over; the remainder are younger

and disabled. | Source: Kaiser Family Foundation

The bankruptcy project is a long-running effort now led by Professor Thorne;

Professor Lawless; Pamela Foohey, a law professor at Indiana University; and

Katherine Porter, a law professor at the University of California, Irvine. The

project — which is financed by their universities — collects and analyzes court

records on a continuing basis and follows up with written questionnaires.

Their latest study —which was posted online on Sunday and has been submitted to

an academic journal for peer review — is based on a sample of personal

bankruptcy cases and questionnaires completed by 895 filers ages 19 to 92.

The questionnaire asked filers what led them to seek bankruptcy protection. Much

like the broader population, people 65 and older usually cited multiple factors.

About three in five said unmanageable medical expenses played a role. A little

more than two-thirds cited a drop in income. Nearly three-quarters put some

blame on hounding by debt collectors.

The study does not delve into those underlying factors, but separate data

provides some insight. The median household led by someone 65 or older had

liquid savings of $60,600 in 2016, according to the Employee Benefit Research

Institute, whereas the bottom 25 percent of households had saved at most $3,260.

That doesn’t provide much of a financial cushion for a catastrophic health

problem. Older Americans typically turn to Medicare to pay their medical bills.

But gaps in coverage, high premiums and requirements that patients shoulder some

costs force many lower-income beneficiaries to spend more of their own income on

those bills, the Kaiser Family Foundation found.

By 2013, the average Medicare beneficiary’s out-of-pocket spending on health

care consumed 41 percent of the average Social Security check, according to

Kaiser, which also estimated that the figure would rise.

More people are also entering their later years carrying debt. For many of them,

at least some of the debt is a mortgage — roughly 41 percent in 2016, compared

with 21 percent in 1989, according to an Urban Institute analysis.

And those who are carrying debt into retirement are carrying more than members

of earlier generations, an analysis by the Employee Benefit Research Institute

found.

Perhaps not surprisingly, the lowest-income households led by individuals 55 or

older carry the highest debt loads relative to their income. More than 13

percent of such households face debt payments that equal more than 40 percent of

their income, nearly double the percentage of such families in 1991, the

employee benefit institute found.

Older Americans’ finances are also being strained by the needs of those around

them.

A little more than a third of the older filers who answered the researchers’

questionnaire said that helping others, like children or older parents, had

contributed to their seeking bankruptcy protection. Marc Stern, a bankruptcy

lawyer in Seattle, said he had seen the phenomenon again and again.

Some parents, Mr. Stern said, had co-signed loans for $10,000 or $20,000 for

adult children and suddenly could no longer afford them. “When you are living on

$2,000 a month and that includes Social Security — and you have rent and savings

are minuscule — it is extremely difficult to recover from something like that,”

he said.

Others had co-signed their children’s student loans. “I never saw parents with

student loans 20 or 30 years ago,” Mr. Stern said.

“It is not uncommon to see student loans of $100,000,” he added. “Then, you see

parents who have guaranteed some of these loans. They are no longer working, and

they have these student loans that are difficult if not impossible to pay or

discharge in bankruptcy, and these are the kids’ loans.”

Keith Morris, chief executive of Elder Law of Michigan, which runs a legal

hotline for older adults, said the prospect of bankruptcy was a regular topic

for his callers.

“They worked all of their lives, and did what they were supposed to do,” he

said, “and through circumstances like a late-life divorce or a death of a spouse

or having to raise grandkids, have put them in a situation where they are not

able to make the bills.”

For Lawrence Sedita, a 74-year-old former carpenter now living in Las Vegas, the

problems began when he lost his health insurance about two years ago. He said he

had been on disability since 1991, when a double pack of 12-foot drywall fell on

his head at work.

After his union, the New York City District Council of Carpenters, changed the

eligibility requirements for his medical, dental and prescription drug

insurance, he lost his coverage.

Mr. Sedita, who has Parkinson’s disease, said his medical expenses had risen

exponentially. (A spokesman for the union declined to comment.)

A medication that helps reduce the shaking — a Parkinson’s symptom — rose to

$1,100 every three months from $70, Mr. Sedita said. “I haven’t taken my

medicine in three months since I can’t afford it,” he added.

He said he and his wife, who has cancer, filed for bankruptcy in June after

living off their credit cards for a time. Their financial difficulty, he said,

“has drained everything out of me.”

Doris Burke and Alain Delaquérière contributed research. Graphics by Karl

Russell.

A version of this article appears in print on Aug. 6, 2018, on Page A1 of the

New York edition with the headline: Bankruptcy Booms Among Older Americans as

Safety Net Frays.

WASHINGTON — The United States economy will remain sluggish

for the next few years, with unemployment high, but budget deficits are starting

to come down, the Congressional Budget Office said on Tuesday in its latest

formal outlook.

The deficit in the current fiscal year is expected to be $1.1 trillion, the

budget office said, the fourth year in which it would exceed $1 trillion.

But it just might be the last such year, at least for a while. Unless Congress

passes new legislation changing the course on spending or taxation — changes

that are a distinct possibility, but no basis for a forecast — projected

deficits would “drop markedly” starting next year and for a decade to come.

That is because current laws would allow the Bush-era tax cuts to expire, the

alternative minimum tax to reach ever more taxpayers and federal spending to

decline modestly under newly imposed spending caps, at least until the aging of

the population and rising costs for health care tilt the balance of spending

upward again.

If Congress leaves current law unchanged, the report said, the deficit will fall

to $585 billion in 2013 and $345 billion in 2014. In other words, doing nothing

might be the most straightforward way for Congress to slash the deficit, a goal

espoused by lawmakers in both parties.

However, the budget office said, such policy — implying higher taxes and

constraints on spending — would crimp economic growth so that the unemployment

rate, now 8.5 percent, would climb to 8.9 percent in the last quarter of this

year and 9.2 percent in the final quarter of 2013.

Representative Eric Cantor of Virginia, the House Republican leader, called the

deficit and unemployment news reason enough for a course change.

“We know that President Obama’s policies have failed to produce the economic

growth needed to pay down these massive deficits that are creating uncertainty,

preventing economic recovery, and harming job creation,” he said. “When

something doesn’t work, you change it. Let’s try something new.”

The report’s economic outlook was a bit gloomier than a year ago both because

the tax increases and spending cuts required under current law would dampen

growth — and because economic troubles abroad may spill over to the U.S.

economy.Douglas W. Elmendorf, director of the Congressional Budget Office, said

that the fiscal tightening “will hold back economic growth” next year, but could

add to the strength of the economy in the long run.

Assuming no change in current law, the budget office expects the economy to grow

2 percent this year and just 1.1 percent in 2013 (measured by the increase in

the gross domestic product, after adjusting for inflation).

As a percentage of gross domestic product, this year’s deficit of $1.1 trillion,

compared with last year’s $1.3 trillion shortfall, “will be 7.0 percent, which

is nearly 2 percentage points below the deficit recorded last year but still

higher than any deficit between 1947 and 2008,” the annual report said. “Over

the next few years, projected deficits in C.B.O.’s baseline drop markedly,

averaging 1.5 percent of G.D.P. over the 2013-2022 period.”

In the next few years, the deficit would still drop below $1 trillion and

decline as a percentage of GDP even if Congress extended the Bush tax cuts and

reversed other budget-balancing policies, according to the office’s alternative

scenario, which uses assumptions other than the status quo. But the improvements

would be less pronounced and would not endure as long.

The improving but still tepid performance of its baseline projection is

reflected, too, in the share of the gross domestic product taken up by the

national debt.

“With deficits small relative to the size of the economy, debt held by the

public drops — from about 75 percent of G.D.P. in 2013 to 62 percent in 2022,

which is still higher than in any year between 1952 and 2009.”

Some say that this year — or perhaps next year, after the election — changes are

virtually certain to occur, one way or another.

Even under current law, the budget office said, the government will need to

continue borrowing to fill the gap between spending and revenues, and the total

federal debt — the accumulated total of such borrowing — will rise to $21.6

trillion in 2022, from its current level of $15.2 trillion. And net interest

payments on the debt would nearly triple, to $624 billion, the report said.

The budget office said it would cost $5.4 trillion to continue major tax cuts

enacted in 2001 and 2003 under President George W. Bush and scheduled to expire

at the end of this year. President Obama and some Democrats want to continue

many of those cuts for individuals with incomes under $200,000 a year and

couples with incomes under $250,000 a year.

Many lawmakers say Congress must block impending cuts in Medicare payments to

doctors, who face a 27 percent reduction in fees in March. Just to maintain

Medicare payment rates at current levels, without an increase, would cost $372

billion over 10 years, compared with spending expected under current law, the

budget office said.

The number of people receiving Social Security disability benefits has been

increasing in recent years, and the budget office predicts that the disability

trust fund will run out of money in 2016.

In addition, the budget office estimates that Medicare’s hospital insurance

trust fund will be exhausted in 2022, two years earlier than the Obama

administration predicted last May. Congress is considering a variety of steps to

slow the growth of Medicare spending, but most provoke sharp disagreement

between Republicans and Democrats.

WASHINGTON

— The Senate voted on Thursday to allow a further increase in the federal debt

limit, permitting President Obama to borrow $1.2 trillion more to operate a

government that spent about 55 percent more than it collected in revenue last

year.

The 52-to-44 vote generally followed party lines, with Democrats supporting the

increase in borrowing authority and Republicans opposed.

In the House last week, Republicans passed a “resolution of disapproval” to stop

the increase in the debt limit. But the Senate refused on Thursday to take up

that measure.

The upshot is that the debt limit will rise immediately to $16.4 trillion, from

the current ceiling of $15.2 trillion.

House Republicans, led by Speaker John A. Boehner, boast that they have changed

the conversation in Washington so that lawmakers focus on how to cut spending.

But Senator Tom Coburn, Republican of Oklahoma, complained that the Senate was

allowing the debt limit to rise in a perfunctory way, with little debate.

“Little has changed in Washington in the last five years,” Mr. Coburn said.

“We’ve argued, debated and lamented on how to rein in the federal government’s

costs and out-of-control spending. All the time that was going on, we were on a

spending binge, spending money we do not have on things we do not need. Even

though we knew we had to borrow more money, Congress has done nothing to avoid

raising the debt limit further. Nothing.”

The 2009 economic stimulus law set the debt limit at $12.1 trillion. Congress

increased the limit in December 2009 and February 2010 and again last summer, as

part of a bipartisan budget agreement.

Senator Max Baucus, Democrat of Montana and chairman of the Finance Committee,

defended the new increase in the debt limit, saying it would not authorize

additional spending, but just ensure that the United States could honor past

commitments.

“Increasing the debt limit permits the Treasury Department to pay the bills we

have already incurred,” Mr. Baucus said.

Senator Richard J. Durbin of Illinois, the No. 2 Senate Democrat, said that many

Republicans who voted against the increase in the debt ceiling had also voted in

recent years to spend more on the wars in Iraq and Afghanistan and on domestic

programs.

Mr. Durbin admonished his colleagues: “Don’t vote for the spending if you won’t

vote for the borrowing, because we know now that they are linked together. They

are one and the same.”

In an address to Congress in February 2009, a week after signing the economic

stimulus law, Mr. Obama said he would “cut the deficit in half by the end of my

first term in office.”

Republicans said Thursday that Mr. Obama was far from that goal. The deficit —

$1.3 trillion in each of the last two fiscal years — has declined slightly from

2009, when it totaled $1.4 trillion.

The federal budget deficit is the difference between money spent and money

collected by the government in a single year, while the debt represents amounts

borrowed by the government over many years to fill those gaps.

With the latest increase in the debt limit, Republicans said, the debt will

cross a significant threshold, as it will be roughly the same size as the

economy, measured by the gross domestic product.

About two-thirds of the debt is held by the public in the form of Treasury

bills, notes and bonds. The rest consists mainly of special-issue government

securities held by trust funds for Social Security, Medicare and other programs.

The Treasury still finds that it can borrow at extraordinarily low interest

rates. But Senator Orrin G. Hatch, Republican of Utah, said the United States

should learn from the experiences of European countries that spent beyond their

means.

“Catastrophic.” “Calamitous.” “Major crisis.” “Self-inflicted wound.” Those are

some of the ways Ben Bernanke, the chairman of the Federal Reserve, has

described the fallout if Congress fails to raise the debt limit by the Aug. 2

deadline.

In Congressional testimony this week, Mr. Bernanke also warned that the Fed

would not be able to fully counter the damage from a default, including the

possibility that spiking interest rates would roil borrowers worldwide and

worsen the federal budget deficit by making it costlier to finance the nation’s

debt.

That’s not all of it. Brinkmanship over the debt limit is only one of many epic

economic policy blunders now in the making. Even if lawmakers raise the debt

limit on time, the economy is weak and getting weaker, as evidenced by slowing

growth and rising unemployment.

Instead of coming up with policies to strengthen the economy, the Republicans

are demanding deep, immediate spending cuts, which would only add to current

weakness. The White House, meanwhile, has suggested cuts should be phased in

slowly and has said that more near-term help would be good for the economy. That

is a better approach. But President Obama has done too little to argue the case,

on Capitol Hill or with the public.

Upfront spending cuts could make sense if the budget deficit were the cause of

the current economic weakness. If it were, interest rates would be rising, not

at generational lows, as the government competed with the private sector. The

real cause is lack of consumer demand in the face of stagnant wages, job

uncertainty and the continuing payback of household debt from the bubble years.

Without strong and steady consumer demand, businesses will not hire, and a

self-sustaining recovery cannot take hold.

In such a situation, government must fill the gap with spending on relief and

recovery measures. Premature spending cuts will only make things worse by

pulling dollars out of a frail economy. Contrary to the claims of Republicans,

and some Democrats, that the nation cannot afford new spending, the government

could, and should, borrow cheaply at today’s low rates in an effort to bolster

demand and, by extension, support jobs.

A place to start would be to extend what little stimulus remains on the books,

including the $57 billion-a-year federal unemployment insurance program and the

$112 billion payroll tax cut for employees. Both are scheduled to expire at the

end of 2011, despite the fact that conditions have deteriorated since they were

enacted last year.

Another crucial step would be to reauthorize the highway trust fund, at least at

existing levels. The fund, which is paid for mainly by the federal gasoline tax,

will allocate $53 billion to states in 2011 for roads and mass transit,

supporting millions of jobs. The House version of the highway bill calls for

deep cuts, and the better Senate version has not garnered enough Republican

support to pass.

It is also past time for lawmakers to move forward with plans for a federal

infrastructure bank to provide seed money for major public works.

In his testimony, Mr. Bernanke emphasized that the deficit was a serious

problem, but not an immediate one. He is right. It can be solved over time, with

spending cuts and tax increases, as the economy recovers.

Recovery, however, requires the creation of millions more jobs, starting now,

than the current economy is capable of generating. It is time for the government

to step up. If it doesn’t, the weakening economy is bound to become even weaker.

WASHINGTON | Sun May 15, 2011

9:52am EDT

Reuters

By Jeff Mason

WASHINGTON (Reuters) - President Barack Obama warned Congress that failing to

raise the debt limit could lead to a worse financial crisis and economic

recession than 2008-09 if investors began doubting U.S. credit-worthiness.

In remarks recorded last week and broadcast by CBS News on Sunday, Obama

repeated his stance that Republicans should not link the debt ceiling decision

to spending cuts as part of deficit-reducing measures.

"If investors around the world thought that the full faith and credit of the

United States was not being backed up, if they thought that we might renege on

our IOUs, it could unravel the entire financial system," Obama told a CBS News

town-hall meeting.

"We could have a worse recession than we already had, a worse financial crisis

than we already had."

The White House and congressional Republicans are locked in a debate over the

deficit and the debt ceiling.

The Treasury Department is expected to hit its $14.3 trillion borrowing limit on

Monday, making it unable to access bond markets again.

Republican leaders, who have said they agree the limit must be raised, say they

will not approve a further increase in borrowing authority without steps to keep

debt under control.

A deal may not emerge for several months.

The Treasury Department says it can stave off default until August 2 by drawing

on other sources of money to pay its bills.

Obama said he was committed to deficit reduction but discouraged a link between

that and the debt limit.

"Let's not have the kind of linkage where we're even talking about not raising

the debt ceiling. That's going to get done," he said. "But let's get serious

about deficit reduction."

A report from the think tank Third Way to be released on Monday supports Obama's

warnings. It says the United States could plunge back into recession if inaction

in Washington forced a debt default, with some 640,000 U.S. jobs vanishing,

stocks falling and lending activity tightening.

Vice President Joe Biden is leading talks between the White House and lawmakers

over how to reduce massive U.S. budget deficits and raise the credit limit. He

told reporters on Thursday that progress was being made but it was too early to

be optimistic about a deal.

At a recent

gathering of House Republicans, lawmakers made it clear that they intend to hold

an increase in the nation’s debt limit hostage to major spending cuts.

Clearly, the Republican aim is to demonstrate their fiscal prudence, as well as

their new political power in the Republican-controlled House. Don’t be fooled.

When it comes to debating the debt limit the facts matter little. It’s all about

posturing.

The debt limit is a cap set by Congress on the amount the nation can legally

borrow. The current limit, $14.3 trillion, will be hit sometime this spring.

Unless Congress raises it before then, the government will have to resort to

temporary tactics, like freeing up money to pay current bills by delaying

payments to federal retirement funds. The longer a standoff endures, the worse

the choices are. For instance, the government might defer other payments, like

tax refunds, as it husbands resources to avoid a default on the public debt.

All that would surely be disruptive and could be disastrous if the nation’s

creditors began to doubt America’s reliability.

The debt limit is a political tool, not a fiscal one. First enacted in 1917, it

was intended to make lawmakers think twice before voting for tax cuts and

spending increases that run up the debt. Unfortunately, it has never worked that

way. Federal debt is high despite the limit because lawmakers repeatedly enter

into expensive and recurring obligations without a plan to pay for them — in

recent years that includes two wars, the George W. Bush-era tax cuts and the

Medicare drug benefit.

As the costs pile up, the debt limit must be increased — not to make room for

new spending, but to raise money to pay for past commitments.

It is, of course, utterly disingenuous to vote for policies that drive up the

debt and then rail against raising the debt limit when the bills come due. It is

akin to piling up purchases on credit and then threatening to bounce the payment

check. But that is what Republicans are saying they will do unless they win deep

cuts in future spending in exchange for a debt-limit increase today. So much for

fiscal prudence.

A better approach would be to pay for legislation when it is enacted, generally

by raising taxes or cutting other spending. The new House leadership has

rejected that approach when it comes to their No. 1 priority: cutting taxes.

They have passed new budget rules that allow taxes to be cut without offsets to

replace the lost revenue. The new rules also forbid raising taxes to pay for

major new spending, like Medicare expansions, requiring instead that any such

spending be offset by cutting other programs. That is a recipe for fiscal

irresponsibility.

House Republican leaders have not said which spending cuts they will demand for

a debt-limit increase. They know that voters don’t want to hear about losing

college aid, environmental safeguards or investor protections. They may try to

call for overall spending caps that would let them take credit for spending

reductions without explaining or defending particular cuts.

What is known is that deep immediate spending cuts would be unwise at a time

when the economy and so many Americans are still struggling. President Obama and

Congressional Democrats need to push back by challenging House Republicans on

the hypocrisy of their new budget rules and by making it clear that playing

games with the debt limit is irresponsible.

January 26,

2011

The New York Times

Filed at 11:58 p.m. EST

By THE ASSOCIATED PRESS

WASHINGTON

(AP) — Far from slowing, the government's deficit spending will surge to a

record $1.5 trillion flood of red ink this year, congressional budget experts

estimated Wednesday, blaming the slow economic recovery and last month's tax-cut

law.

The report was sobering new evidence that it will take more than President

Barack Obama's proposed freeze on some agencies to stem the nation's

extraordinary budget woes. Republicans say they want big budget cuts but so far

are light on specifics.

Wednesday's Congressional Budget Office estimates indicate the government will

have to borrow 40 cents for every dollar it spends this fiscal year, which ends

Sept. 30. Tax revenues are projected to drop to their lowest levels since 1950,

when measured against the size of the economy.

The report, full of nasty news, also says that after decades of Social Security

surpluses, the vast program's costs are no longer covered by payroll taxes.

The budget estimates will add fuel to the already-raging debate over spending

and looming legislation that would allow the government to borrow more money as

the national debt nears the $14.3 trillion cap set by law. Republicans

controlling the House say there's no way they'll raise the limit without

significant budget cuts, starting with a government funding bill that will

advance next month.

Democrats and Republicans agree that stern anti-deficit steps are needed, but

neither Obama nor his resurgent GOP rivals on Capitol Hill are — so far —

willing to put on the table cuts to popular benefit programs such as Medicare,

farm subsidies and Social Security. The need to pass legislation to fund the

government and prevent a first-ever default on U.S. debt obligations seems sure

to drive the two sides into negotiations.

Though the analysis predicts the economy will grow by 3.1 percent this year, it

foresees unemployment remaining above 9 percent.

Dauntingly for Obama, the nonpartisan agency estimates a nationwide jobless rate

of 8.2 percent on Election Day in 2012. That's higher that the rates that

contributed to losses by Presidents Jimmy Carter (7.5 percent) and George H.W.

Bush (7.4 percent). The nation isn't projected to be at full employment —

considered to be a jobless rate of about 5 percent — until 2016.

The latest deficit figures are up from previous estimates because of bipartisan

legislation passed in December that extended George W. Bush-era tax cuts and

unemployment benefits for the long-term jobless and provided a 2 percentage

point Social Security payroll tax cut this year.

That measure added almost $400 billion to this year's deficit, CBO says.

The deficit is on track to beat the record of $1.4 trillion set in 2009. The

budget experts predict the deficit will drop to $1.1 trillion next year, still

very high by historical standards.

Republicans focus on Obama's contributions to the deficit: his $821 billion

economic stimulus plan, boosts for domestic programs and his signature health

care overhaul. Obama points out that he inherited deficits that would have

exceeded $1 trillion a year anyway.

The chilling figures came the day after Obama called for a five-year freeze on

optional spending in domestic agency budgets passed by Congress each year.

Republicans were quick to blame Obama for the rising red ink. Rep. Jeb

Hensarllng of Texas, chairman of the House Republican Conference, said the

report "paints a picture that is more dangerous than most Americans could

anticipate."

"What is our leader in the White House doing about it? Asking Congress to raise

the debt ceiling, proposing new spending and sticking future generations with a

multi-trillion dollar tab," Hensarling said.

Democrat Kent Conrad, chairman of the Senate Budget Committee, pointed to a

problem lawmakers are sure to keep facing:

"When the American people are asked what they want done and to prioritize what

they want, they want the deficits and debt dealt with. But when they are asked

very specifically, will they support changes in Social Security, the polls say

no. Changes in Medicare? The polls say no. Changes in defense spending? The

polls say no."

"I would've liked very much if the president would have spent a bit more time

helping the American people understand how really big this problem is," added

Conrad, D-N.D.

Republicans are calling for deeper cuts for education, housing and the FBI —

among many programs — to return them to the 2008 levels in place before Obama

took office.

But those nondefense programs make up just 12 or so percent of the $3.7 trillion

budget, which means any upcoming deficit reduction package — at least one that

begins to significantly slow the gush of red ink — will require politically

dangerous curbs to popular benefit programs. That includes Social Security,

Medicare, the Medicaid health care program for the poor and disabled, and food

stamps.

Neither Obama nor his GOP rivals on Capitol Hill have yet come forward with

specific proposals for cutting such benefit programs. Successful efforts to curb

the deficit always require active, engaged presidential leadership, but Obama's

unwillingness to thus far take chances has deficit hawks discouraged. Obama will

release his 2012 budget proposal next month.

"The proposals we've seen so far from the president and congressional

Republicans amount to little more than tinkering around the edges," said Concord

Coalition Executive Director Bob Bixby.

"Somebody is going to have to bite the bullet and get this process going," said

Maya MacGuineas of the Committee for a Responsible Federal Budget, a bipartisan

group that advocates fiscal responsibility. "And that somebody has to be the

president."

Obama has steered clear of the recommendations of his deficit commission, which

in December called for difficult moves such as increasing the Social Security

retirement age and reducing future increases in benefits. It also proposed a

15-cents-a-gallon increase in the gasoline tax and eliminating or scaling back

tax breaks — including the child tax credit, mortgage interest deduction and

deduction claimed by employers who provide health insurance — in exchange for

rate cuts on corporate and income taxes.

CBO predicts that the deficit will fall to $551 billion by 2015 — a sustainable

3 percent of the economy — but only if the Bush tax cuts are wiped off the

books. Under its rules, CBO assumes the recently extended cuts in taxes on

income, investment and people inheriting large estates will expire in two years.

If those tax cuts, and numerous others, are extended, the deficit for that year

would be almost three times as large.

Tax revenues, which dropped significantly in 2009 because of the recession, have

stabilized. But revenue growth will continue to be constrained. CBO projects

revenues to be 6 percent higher in 2011 than they were two years ago, which will

not keep pace with the growth in spending.

• City expected November budget deficit

of less than £17.4bn

• Analysts warn trend points to a deficit

of £155bn for the year

Tuesday 21 December 2010

18.20 GMT

Guardian.co.uk

Larry Elliott

Economics editor

This article was published on guardian.co.uk

at 18.20 GMT on Tuesday 21 December 2010.

A version appeared on p21 of the Main section section

of the Guardian on Wednesday 22 December 2010.

It was last modified at 00.01 GMT

on Wednesday 22 December 2010.

George Osborne received a blow as it emerged that state borrowing soared to

the highest on record for a single month despite the government's austerity

measures to rein in the deficit.

News that higher spending on defence, the NHS and contribution to the European

Union had left Britain in the red by £23.3bn stunned the City, which had been

expecting the early fruits from the chancellor's spending restraint to cut the

deficit from the £17.4bn recorded in November 2009.

Sterling dipped to its lowest level against the US dollar in three months

following the release of the official data amid fears that the coalition would

struggle to meet its targets for reducing a deficit that rose sharply during the

longest and deepest recession Britain has suffered since the interwar period.

Figures from the Office for National Statistics showed that despite robust

economic growth in the second and third quarters of 2010, public borrowing has

shown virtually no improvement on last year. In the first eight months of the

2010-11 financial year, net borrowing stood at £104.4bn, compared with £105.1bn

in the same period of 2009-10.

Analysts said the public finances tended to be volatile from month to month, and

that it was possible that the highest monthly deficit since modern records began

in 1993 was a freak. They added, however, that if the trend seen so far

continued, the deficit was likely to total £155bn by the end of the financial

year, £7bn higher than predicted by the government's fiscal watchdog, the Office

for Budget Responsibility.

Today's borrowing figures were the third disappointing piece of news in the past

week for the government, following the surprise increase in inflation and the

rise in unemployment to more than 2.5m.

The City and academic economists believe growth in the final three months of

2010 is unlikely to match the 0.8% seen in the third quarter, and that activity

will weaken further in early 2010.

Osborne believes that the poor state of the public finances vindicates his

decision to announce the biggest four-year fiscal squeeze since the second world

war. "November's borrowing figures show why the government has had to take

decisive action to take Britain out of the financial danger zone," a Treasury

spokesman said.

David Kern, Chief Economist at the British Chambers of Commerce (BCC), said:

"These figures are much worse than expected and show a significant increase in

the deficit compared with the same month a year ago. Britain's fiscal position

is very serious and it is essential for the government to implement its tough

strategy aimed at stabilising our public finances.

"British business supports these measures and wants to see the government

continuing to focus on spending cuts rather than tax rises. But, in order for

this policy to be successful the austerity measures must be supplemented by a

credible growth strategy so that businesses can drive a lasting recovery."

Michael Derks, chief strategist at FxPro, said: "More than anything, these

figures reinforce just how important fiscal consolidation is, and reiterates how

hard the process can be. The much-vaunted spending restraint that formed such a

critical part of the Chancellor's fiscal austerity has not started, based on

these latest figures. The pound may give the chancellor a couple more months'

leeway on the spending side, but thereafter it will want to see hard evidence

that restraint is actually working."

A breakdown of the ONS figures showed that spending in the first eight months of

the year was 6.8% up on the same period of 2009-10, compared to the 6% growth

projected by the Treasury. "Some departments may have to trim their spending in

the months ahead to stay within planned levels," said Stephen Lewis of Monument

Securities. "There is a risk, as a result, public services will suffer, in a way

that could erode popular support for the coalition's policies. In such

circumstances, it could become more difficult for the coalition to hold

together. These uncertainties are likely to be reflected increasingly in risk

premiums in sterling asset markets."

June 18, 2010

The New York Times

By PETER S. GOODMAN

PALM BEACH, Fla. — For the companies that promise relief to Americans

confronting swelling credit card balances, these are days of lucrative

opportunity.

So lucrative, that an industry trade association, the United States

Organizations for Bankruptcy Alternatives, recently convened here, in the

oceanfront confines of the Four Seasons Resort, to forge deals and plot

strategy.

At a well-lubricated evening reception, a steel drum band played Bob Marley

songs as hostesses in skimpy dresses draped leis around the necks of arriving

entrepreneurs, some with deep tans.

The debt settlement industry can afford some extravagance. The long recession

has delivered an abundance of customers — debt-saturated Americans, suffering

lost jobs and income, sliding toward bankruptcy. The settlement companies

typically harvest fees reaching 15 to 20 percent of the credit card balances

carried by their customers, and they tend to collect upfront, regardless of

whether a customer’s debt is actually reduced.

State attorneys general from New York to California and consumer watchdogs like

the Better Business Bureau say the industry’s proceeds come at the direct

expense of financially troubled Americans who are being fleeced of their last

dollars with dubious promises.

Consumers rarely emerge from debt settlement programs with their credit card

balances eliminated, these critics say, and many wind up worse off, with

severely damaged credit, ceaseless threats from collection agents and lawsuits

from creditors.

In the Kansas City area, Linda Robertson, 58, rues the day she bought the pitch

from a debt settlement company advertising on the radio, promising to spare her

from bankruptcy and eliminate her debts. She wound up sending nearly $4,000 into

a special account established under the company’s guidance before a credit card

company sued her, prompting her to drop out of the program.

By then, her account had only $1,470 remaining: The debt settlement company had

collected the rest in fees. She is now filing for bankruptcy.

“They take advantage of vulnerable people,” she said. “When you’re desperate and

you’re trying to get out of debt, they take advantage of you.” Debt settlement

has swollen to some 2,000 firms, from a niche of perhaps a dozen companies a

decade ago, according to trade associations and the Federal Trade Commission,

which is completing new rules aimed at curbing abuses within the industry.

Last year, within the industry’s two leading trade associations — the United

States Organizations for Bankruptcy Alternatives and the Association of

Settlement Companies — some 250 companies collectively had more than 425,000

customers, who had enrolled roughly $11.7 billion in credit card balances in

their programs.

As the industry has grown, so have allegations of unfair practices. Since 2004,

at least 21 states have brought at least 128 enforcement actions against debt

relief companies, according to the National Association of Attorneys General.

Consumer complaints received by states more than doubled between 2007 and 2009,

according to comments filed with the Federal Trade Commission.

“The industry’s not legitimate,” said Norman Googel, assistant attorney general

in West Virginia, which has prosecuted debt settlement companies. “They’re

targeting a group of people who are already drowning in debt. We’re talking

about middle-class and lower middle-class people who had incomes, but they were

using credit cards to survive.”

The industry counters that a few rogue operators have unfairly tarnished the

reputations of well-intentioned debt settlement companies that provide a crucial

service: liberating Americans from impossible credit card burdens.

With the unemployment rate near double digits and 6.7 million people out of work

for six months or longer, many have relied on credit cards. By the middle of

last year, 6.5 percent of all accounts were at least 30 days past due, up from

less than 4 percent in 2005, according to Moody’s Economy.com.

Yet a 2005 alteration spurred by the financial industry made it harder for

Americans to discharge credit card debts through bankruptcy, generating demand

for alternatives like debt settlement.

The Arrangement

The industry casts itself as a victim of a smear campaign orchestrated by the

giant banks that dominate the credit card trade and aim to hang on to the

spoils: interest rates of 20 percent or more and exorbitant late fees.

“We’re the little guys in this,” said John Ansbach, the chief lobbyist for the

United States Organizations for Bankruptcy Alternatives, better known as Usoba

(pronounced you-SO-buh). “We exist to advocate for consumers. Two and a half

billion dollars of unsecured debt has been settled by this industry, so how can

you take the position that it has no value?”

But consumer watchdogs and state authorities argue that debt settlement

companies generally fail to deliver.

In the typical arrangement, the companies direct consumers to set up special

accounts and stock them with monthly deposits while skipping their credit card

payments. Once balances reach sufficient size, negotiators strike lump-sum

settlements with credit card companies that can cut debts in half. The programs

generally last two to three years.

“What they don’t tell their customers is when you stop sending the money,

creditors get angry,” said Andrew G. Pizor, a staff lawyer at the National

Consumer Law Center. “Collection agents call. Sometimes they sue. People think

they’re settling their problems and getting some relief, and lo and behold they

get slammed with a lawsuit.”

In the case of two debt settlement companies sued last year by New York State,

the attorney general alleged that no more than 1 percent of customers gained the

services promised by marketers. A Colorado investigation came to a similar

conclusion.

The industry’s own figures show that clients typically fail to secure relief. In

a survey of its members, the Association of Settlement Companies found that

three years after enrolling, only 34 percent of customers had either completed

programs or were still saving for settlements.

“The industry is designed almost as a Ponzi scheme,” said Scott Johnson, chief

executive of US Debt Resolve, a debt settlement company based in Dallas, which

he portrays as a rare island of integrity in a sea of shady competitors.

“Consumers come into these programs and pay thousands of dollars and then

nothing happens. What they constantly have to have is more consumers coming into

the program to come up with the money for more marketing.”

The Pitch

Linda Robertson knew nothing about the industry she was about to encounter when

she picked up the phone at her Missouri home in February 2009 in response to a

radio ad.

What she knew was that she could no longer manage even the monthly payments on

her roughly $23,000 in credit card debt.

So much had come apart so quickly.

Before the recession, Ms. Robertson had been living in Phoenix, earning as much

as $8,000 a month as a real estate appraiser. In 2005, she paid $185,000 for a

three-bedroom house with a swimming pool and a yard dotted with hibiscus.

When the real estate business collapsed, she gave up her house to foreclosure

and moved in with her son. She got a job as a waitress, earning enough to hang

on to her car. She tapped credit cards to pay for gasoline and groceries.

By late 2007, she and her son could no longer afford his apartment. She moved

home to Kansas City, where an aunt offered a room. She took a job on the night

shift at a factory that makes plastic lids for packaged potato chips, earning

$11.15 an hour.

Still, her credit card balances swelled.

The radio ad offered the services of a company based in Dallas with a soothing

name: Financial Freedom of America. It cast itself as an antidote to the

breakdown of middle-class life.

“We negotiate the past while you navigate the future,” read a caption on its Web

site, next to a photo of a young woman nose-kissing an adorable boy. “The

American Dream. It was never about bailouts or foreclosures. It was always about

American values like hard work, ingenuity and looking out for your neighbor.”

When Ms. Robertson called, a customer service representative laid out a plan.

Every month, Ms. Robertson would send $427.93 into a new account. Three years

later, she would be debt-free. The representative told her the company would

take $100 a month as an administrative fee, she recalled. His tone was

take-charge.

“You talk about a rush-through,” Ms. Robertson said. “I didn’t even get to read

the contract. It was all done. I had to sign it on the computer while he was on

the phone. Then he called me back in 10 minutes to say it was done. He made me

feel like this was the answer to my problems and I wasn’t going to have to face

bankruptcy.”

Ms. Robertson made nine payments, according to Financial Freedom. Late last

year, a sheriff’s deputy arrived at her door with court papers: One of her

creditors, Capital One, had filed suit to collect roughly $5,000.

Panicked, she called Financial Freedom to seek guidance. “They said, ‘Oh, we

don’t have any control over that, and you don’t have enough money in your

account for us to settle with them,’ ” she recalled.

Her account held only $1,470, the representative explained, though she had by

then deposited more than $3,700. Financial Freedom had taken the rest for its

administrative fees, the company confirmed.

Financial Freedom later negotiated for her to make $100 monthly payments toward

satisfying her debt to the creditor, but Ms. Robertson rejected that

arrangement, no longer trusting the company. She demanded her money back.

She also filed a report with the Better Business Bureau in Dallas, adding to a

stack of more than 100 consumer complaints lodged against the company. The

bureau gives the company a failing grade of F.

Ms. Robertson received $1,470 back through the closure of her account, and then

$1,120 — half the fees that Financial Freedom collected. Her pending bankruptcy

has cost her $1,500 in legal fees.

“I trusted them,” she said. “They sounded like they were going to help me out.

It’s a rip-off.”

Financial Freedom’s chief executive, Corey Butcher, rejected that

characterization.

“We talked to her multiple times and verified the full details,” he said, adding

that his company puts every client through a verification process to validate

that they understand the risks — from lawsuits to garnished wages.

Intense and brooding, Mr. Butcher speaks of a personal mission to extricate

consumers from credit card debt. But roughly half his customers fail to complete

the program, he complained, with most of the cancellations coming within the

first six months. He pinned the low completion rate on the same lack of

discipline that has fostered many American ailments, from obesity to the

foreclosure crisis.

“It comes from a lack of commitment,” Mr. Butcher said. “It’s like going and

hiring a personal trainer at a health club. Some people act like they have lost

the weight already, when actually they have to go to the gym three days a week,

use the treadmill, cut back on their eating. They have to stick with it. At some

point, the client has to take responsibility for their circumstance.”

Consumer watchdogs point to another reason customers wind up confused and upset:

bogus marketing promises.

In April, the United States Government Accountability Office released a report

drawing on undercover agents who posed as prospective customers at 20 debt

settlement companies. According to the report, 17 of the 20 firms advised

clients to stop paying their credit card bills. Some companies marketed their

programs as if they had the imprimatur of the federal government, with one

advertising itself as a “national debt relief stimulus plan.” Several claimed

that 85 to 100 percent of their customers completed their programs.

“The vast majority of companies provided fraudulent and deceptive information,”

said Gregory D. Kutz, managing director of forensic audits and special

investigations at the G.A.O. in testimony before the Senate Commerce Committee

during an April hearing.

At the same hearing, Senator Claire McCaskill, a Missouri Democrat, pressed Mr.

Ansbach, the Usoba lobbyist, to explain why his organization refused to disclose

its membership.

“The leadership in our trade group candidly was concerned that publishing a list

of members ended up being a subpoena list,” Mr. Ansbach said.

“Probably a genuine concern,” Senator McCaskill replied.

The Coming Crackdown

On multiple fronts, state and federal authorities are now taking aim at the

industry.

The Federal Trade Commission has proposed banning upfront fees, bringing

vociferous lobbying from industry groups. The commission is expected to issue

new rules this summer. Senator McCaskill has joined with fellow Democrat Charles

E. Schumer of New York to sponsor a bill that would cap fees charged by debt

settlement companies at 5 percent of the savings recouped by their customers.

Legislation in several states, including New York, California and Illinois,

would also cap fees. A new consumer protection agency created as part of the

financial regulatory reform bill in Congress could further constrain the

industry.

The prospect of regulation hung palpably over the trade show at this

Atlantic-side resort, tempering the orchid-adorned buffet tables and poolside

cocktails with a note of foreboding.

“The current debt settlement business model is going to die,” declared Jeffrey

S. Tenenbaum, a lawyer in the Washington firm Venable, addressing a packed

ballroom. “The only question is who the executioner is going to be.”

That warning did not dislodge the spirit of expansion. Exhibitors paid as much

as $4,500 for display space to showcase their wares — software to manage

accounts, marketing expertise, call centers — to attendees who came for two days

of strategy sessions and networking.

Cody Krebs, a senior account executive from Southern California, manned a booth

for LowerMyBills.com, whose Internet ads link customers to debt settlement

companies. Like many who have entered the industry, he previously sold subprime

mortgages. When that business collapsed, he found refuge selling new products to

the same set of customers — people with poor credit.

“It’s been tremendous,” he said. “Business has tripled in the last year and a

half.”

The threat of regulations makes securing new customers imperative now, before

new rules can take effect, said Matthew G. Hearn, whose firm, Mstars of

Minneapolis, trains debt settlement sales staffs. “Do what you have to do to get

the deals on the board,” he said, pacing excitedly in front of a podium.

And if some debt settlement companies have gained an unsavory reputation, he

added, make that a marketing opportunity.

“We aren’t like them,” Mr. Hearn said. “You need to constantly pitch that. ‘We

aren’t bad actors. It’s the ones out there that are.’ ”

July 3, 2009

Filed at 11:21 a.m. ET

The New York Times

By THE ASSOCIATED PRESS

WASHINGTON (AP) -- The Founding Fathers left one legacy not

celebrated on Independence Day but which affects us all. It's the national debt.

The country first got into debt to help pay for the Revolutionary War. Growing

ever since, the debt stands today at a staggering $11.5 trillion -- equivalent

to over $37,000 for each and every American. And it's expanding by over $1

trillion a year.

The mountain of debt easily could become the next full-fledged economic crisis

without firm action from Washington, economists of all stripes warn.

''Unless we demonstrate a strong commitment to fiscal sustainability in the

longer term, we will have neither financial stability nor healthy economic

growth,'' Federal Reserve Chairman Ben Bernanke recently told Congress.

Higher taxes, or reduced federal benefits and services -- or a combination of

both -- may be the inevitable consequences.

The debt is complicating efforts by President Barack Obama and Congress to cope

with the worst recession in decades as stimulus and bailout spending combine

with lower tax revenues to widen the gap.

Interest payments on the debt alone cost $452 billion last year -- the largest

federal spending category after Medicare-Medicaid, Social Security and defense.

It's quickly crowding out all other government spending. And the Treasury is

finding it harder to find new lenders.

The United States went into the red the first time in 1790 when it assumed $75

million in the war debts of the Continental Congress.

Alexander Hamilton, the first treasury secretary, said, ''A national debt, if

not excessive, will be to us a national blessing.''

Some blessing.

Since then, the nation has only been free of debt once, in 1834-1835.

The national debt has expanded during times of war and usually contracted in

times of peace, while staying on a generally upward trajectory. Over the past

several decades, it has climbed sharply -- except for a respite from 1998 to

2000, when there were annual budget surpluses, reflecting in large part what

turned out to be an overheated economy.

The debt soared with the wars in Iraq and Afghanistan and economic stimulus

spending under President George W. Bush and now Obama.

The odometer-style ''debt clock'' near Times Square -- put in place in 1989 when

the debt was a mere $2.7 trillion -- ran out of numbers and had to be shut down

when the debt surged past $10 trillion in 2008.

The clock has since been refurbished so higher numbers fit. There are several

debt clocks on Web sites maintained by public interest groups that let you watch

hundreds, thousands, millions zip by in a matter of seconds.

The debt gap is ''something that keeps me awake at night,'' Obama says.

He pledged to cut the budget ''deficit'' roughly in half by the end of his first

term. But ''deficit'' just means the difference between government receipts and

spending in a single budget year.

This year's deficit is now estimated at about $1.85 trillion.

Deficits don't reflect holdover indebtedness from previous years. Some spending

items -- such as emergency appropriations bills and receipts in the Social

Security program -- aren't included, either, although they are part of the

national debt.

The national debt is a broader, and more telling, way to look at the

government's balance sheets than glancing at deficits.

According to the Treasury Department, which updates the number ''to the penny''

every few days, the national debt was $11,518,472,742,288 on Wednesday.

The overall debt is now slightly over 80 percent of the annual output of the

entire U.S. economy, as measured by the gross domestic product.

By historical standards, it's not proportionately as high as during World War

II, when it briefly rose to 120 percent of GDP. But it's still a huge liability.

Also, the United States is not the only nation struggling under a huge national

debt. Among major countries, Japan, Italy, India, France, Germany and Canada

have comparable debts as percentages of their GDPs.

Where does the government borrow all this money from?

The debt is largely financed by the sale of Treasury bonds and bills. Even

today, amid global economic turmoil, those still are seen as one of the world's

safest investments.

That's one of the rare upsides of U.S. government borrowing.

Treasury securities are suitable for individual investors and popular with other

countries, especially China, Japan and the Persian Gulf oil exporters, the three

top foreign holders of U.S. debt.

But as the U.S. spends trillions to stabilize the recession-wracked economy,

helping to force down the value of the dollar, the securities become less

attractive as investments. Some major foreign lenders are already paring back on

their purchases of U.S. bonds and other securities.

And if major holders of U.S. debt were to flee, it would send shock waves

through the global economy -- and sharply force up U.S. interest rates.

As time goes by, demographics suggest things will get worse before they get

better, even after the recession ends, as more baby boomers retire and begin

collecting Social Security and Medicare benefits.

While the president remains personally popular, polls show there is rising

public concern over his handling of the economy and the government's mushrooming

debt -- and what it might mean for future generations.

If things can't be turned around, including establishing a more efficient health

care system, ''We are on an utterly unsustainable fiscal course,'' said the

White House budget director, Peter Orszag.

Some budget-restraint activists claim even the debt understates the nation's

true liabilities.

The Peter G. Peterson Foundation, established by a former commerce secretary and

investment banker, argues that the $11.4 trillion debt figures does not take

into account roughly $45 trillion in unlisted liabilities and unfunded

retirement and health care commitments.

That would put the nation's full obligations at $56 trillion, or roughly

$184,000 per American, according to this calculation.

Friday 6 February 2009

10.41 GMT

Guardian.co.uk

Larry Elliott, economics editor

This article was first published on guardian.co.uk

at 10.41 GMT on Friday 6 February 2009.

It was last updated at 10.48 GMT

on Friday 6 February 2009.

Personal bankruptcy hit a record level and company failures soared by 50% as

the collapse in the economy in the final three months of 2008 took its toll,

official figures showed today.

Data from the Insolvency Service revealed that the steepest decline in output in

almost 30 years led to 19,100 people being declared bankrupt - a 22% increase on

the fourth quarter of 2007.

A further 10,000 people took out individual voluntary arrangements (IVAs) under

which interest on debt is frozen in exchange for set repayments each month.

The total of 29,444 people being declared insolvent was up 18.5% on a year

earlier and was higher than during the recession of the early 1990s.

The 1.5% contraction in the economy in the wake of the financial market mayhem

last autumn also claimed 4,607 companies - a 52% increase in liquidations on the

October to December period of 2007.

Economists warned that the level of bankruptcies was set to increase as

unemployment rose and the problems caused by the credit crunch meant people were

no longer able to borrow their way out of trouble.

Howard Archer, chief UK and European Economist at IHS Global Insight, said:

"Unfortunately, the marked rise in the number of individual insolvencies in the

fourth quarter of 2008 is a harbinger of what is very likely to be seen through

2009.

"Deep economic contraction, sharply rising unemployment, higher debt levels,

lower equity prices, and more and more people being trapped in negative equity

will exact an increasing toll over the coming months.

"While the substantial cuts in interest rates by the Bank of England will

obviously help some people, they are likely to be insufficient to save many from

insolvency."

Alan Tomlinson, partner at licensed insolvency practitioners Tomlinsons, said:

"I have been an insolvency practitioner for over 25 years and have never seen so

many companies, from all sectors, going to the wall. Trading conditions have

never been so tough and given the bleak economic outlook it could be some time

yet before they begin to improve.

"The appalling economic conditions are claiming more and more victims, as

companies in all sectors make redundancies or simply fail.

"What is especially interesting is that more people have gone down the

bankruptcy rather than the IVA route, which is a reflection of the fact that

lenders have tightened up the criteria for the acceptance of IVAs."

The Insolvency Service figures also showed a 75% jump in the number of people

declared insolvent in Scotland during the final quarter at 5,807, although the

figure was slightly down on the total for the previous quarter.

In Northern Ireland insolvencies increased by 39% year-on-year to 443 during the

three months to the end of December.

Nick O'Reilly, president of insolvency professionals' trade body R3, said: "What

today's figures mean is that in 2008 we saw a staggering 350 people becoming

insolvent in the UK every day. For 2009 our members believe this number will

reach in excess of 430 people a day for the whole of the UK.

"The outlook is bleak for the next two years, when insolvency practitioners

expect to see in excess of 158,000 personal insolvencies annually.

"We'll start to see the knock-on effects of increasing business failures and

redundancies on personal financial situations."

Sunday 25 January 2009

The Observer

Heather Stewart

This article was first published

on guardian.co.uk at 00.01 GMT

on Sunday 25 January 2009.

It appeared in the Observer

on Sunday 25 January 2009

on p27 of the Focus section.

It was last updated at 00.14 GMT

on Sunday 25 January 2009.

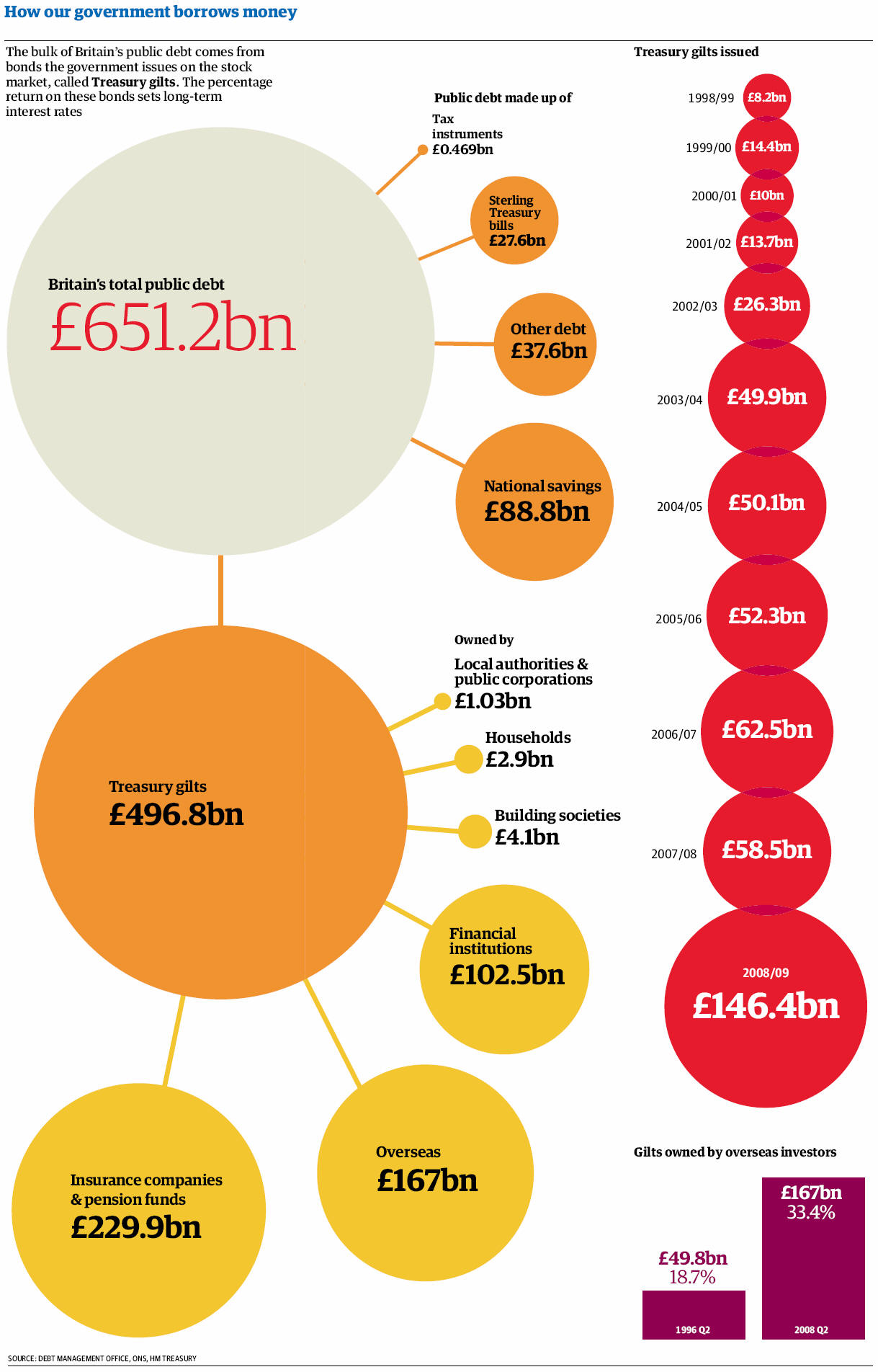

Official figures from last week showed that the government had

run up total debts of £697.5bn, or 47.5% of GDP, by the end of 2008. That

includes just over £100bn for the nationalisation of Northern Rock and the

recapitalisation of Royal Bank of Scotland.

How does that compare with other countries?

Ranked by our debt-to-GDP ratio, we came 18th of 28 members of the Organisation

of Economic Co-operation and Development in 2007, clocking in at 30.4% on the

OECD's measure. A number of other major economies had higher levels of

borrowing: Japan's debt was worth 85.9% of its GDP, for example, and Italy's

well over 100%. Debt levels in many countries are likely to explode in the years

ahead, too, as governments spend billions of dollars on recapitalising their

financial sectors, and boosting public spending to kick-start the economy.

Is the debt mountain about to get much bigger?

Yes: the Office for National Statistics has said that the liabilities of RBS,

thought to be around £1.7tn, will soon have to appear on the government's

balance sheet, because its shareholding, of almost 70%, gives it enough

managerial control over the battered bank to make it a public institution.

However, the minutiae of the statisticians' rules mean that although RBS's

liabilities will turn up on the books, many of its assets - such as the homes on

which mortgages are secured - will not. So the eye-watering debt figures we are

likely to see over the next year are a bit misleading. Even without the banking

rescues, though, public debt has already hit 40.4% of GDP, bursting through the

40% limit the prime minister laid down as one of his fiscal rules when Labour

came to power. And as recession eats away at tax revenues, and the government

spends billions of pounds on Keynesian fiscal stimulus, the chancellor's

forecasts show debt peaking at more than £1tn, or 57.4% of GDP by 2012-13.

What about Alistair Darling's latest bank rescue package?

The government announced last Monday that it would introduce a taxpayer-backed

insurance scheme, allowing the banks to cap their losses on so-called "toxic"

assets, if the loans go sour. That could potentially expose the public to vast

losses and the unknown size of the black hole helped to send sterling into a

tailspin last week. But the Treasury insists that many of the loans will

eventually come good - and the banks are paying the government a fee for its

trouble.

Is Britain at risk of "going bankrupt"?

It is highly unlikely. The government currently borrows about 35% of its total

debts from foreign investors and there is as yet little evidence of them heading

for the door: the German and Greek governments have had more problems borrowing

money in the capital markets in the past few weeks than the UK. However, if

foreign investors do go off gilts, then yields will be driven up - so, in

effect, taxpayers will end up paying higher interest rates to borrow money.

Much of the cash the government needs can continue to be borrowed from taxpayers

at home - pension funds such as government bonds, or gilts, because they can

match the fixed returns against their liabilities, and cash is pouring into

National Savings, which are invested in gilts as nervous savers shun risky

looking banks. If overseas investors lose confidence in the UK, we will have to

fund the debts ourselves, in effect, borrowing from our own future income. That

could prolong the downturn and force the Bank of England to keep interest rates

lower, and for longer, than it otherwise might have done, to compensate for the

tightening of fiscal policy, but it doesn't mean we are "bust".

Will we have to "call in the IMF", as David Cameron claimed last week?

Again, it's not impossible, but highly unlikely: it would only happen if the

government was unable either to meet a debt repayment, or to roll over, or

"refinance" the debt with investors, in the capital markets. Ireland, Turkey and

Greece all look much closer to that extreme than the UK. The verdict of credit

ratings agency Moody's last week was that increasing borrowing in the

short-term, in order to limit the length and severity of the recession, is a

"calculated risk," which it doesn't think endangers the UK's creditworthiness.

Spain and Greece have had their ratings downgraded, however, and Ireland has

been warned that it could face the same fate.

If the problem in the first place was too much borrowing, isn't it dangerous to

try to fix it by borrowing even more?

Yes, but the government believes the risk of allowing the credit markets to

seize up, potentially driving the economy into full-blown depression, is even

greater. As Mervyn King, governor of the Bank of England, put it last week:

"This is the paradox of policy at present - almost any policy measure that is

desirable now appears diametrically opposite to the direction in which we need

to go in the long term."

The collection agencies call at least 20 times a day. For a

little quiet, Diane McLeod stashes her phone in the dishwasher.

But right up until she hit the wall financially, Ms. McLeod was a dream customer

for lenders. She juggled not one but two mortgages, both with interest rates

that rose over time, and a car loan and high-cost credit card debt. Separated

and living with her 20-year-old son, she worked two jobs so she could afford her

small, two-bedroom ranch house in suburban Philadelphia, the Kia she drove to

work, and the handbags and knickknacks she liked.

Then last year, back-to-back medical emergencies helped push her over the edge.

She could no longer afford either her home payments or her credit card bills.

Then she lost her job. Now her home is in foreclosure and her credit profile in

ruins.

Ms. McLeod, who is 47, readily admits her money problems are largely of her own

making. But as surely as it takes two to tango, she had partners in her

financial demise. In recent years, those partners, including the financial

giants Citigroup, Capital One and GE Capital, were collecting interest payments

totaling more than 40 percent of her pretax income and thousands more in fees.

Years of spending more than they earn have left a record number of Americans

like Ms. McLeod standing at the financial precipice. They have amassed a

mountain of debt that grows ever bigger because of high interest rates and fees.

While the circumstances surrounding these downfalls vary, one element is

identical: the lucrative lending practices of America’s merchants of debt have

led millions of Americans — young and old, native and immigrant, affluent and

poor — to the brink. More and more, Americans can identify with miners of old:

in debt to the company store with little chance of paying up.

It is not just individuals but the entire economy that is now suffering.

Practices that produced record profits for many banks have shaken the nation’s

financial system to its foundation. As a growing number of Americans default,

banks are recording hundreds of billions in losses, devastating their

shareholders.

To reduce the risk of a domino effect, the Bush administration fashioned an

emergency rescue plan last week to shore up Fannie Mae and Freddie Mac, the

nation’s two largest mortgage finance companies, if necessary.

To be sure, the increased availability of credit has contributed mightily to the

American economy and has allowed consumers to make big-ticket purchases like

homes, cars and college educations.

But behind the big increase in consumer debt is a major shift in the way lenders

approach their business. In earlier years, actually being repaid by borrowers

was crucial to lenders. Now, because so much consumer debt is packaged into

securities and sold to investors, repayment of the loans takes on less

importance to those lenders than the fees and charges generated when loans are

made.

Lenders have found new ways to squeeze more profit from borrowers. Though

prevailing interest rates have fallen to the low single digits in recent years,

for example, the rates that credit card issuers routinely charge even borrowers

with good credit records have risen, to 19.1 percent last year from 17.7 percent

in 2005 — a difference that adds billions of dollars in interest charges

annually to credit card bills.

Average late fees rose to $35 in 2007 from less than $13 in 1994, and fees